Funding structures for Oakland church acquisition and reuse

Visuals

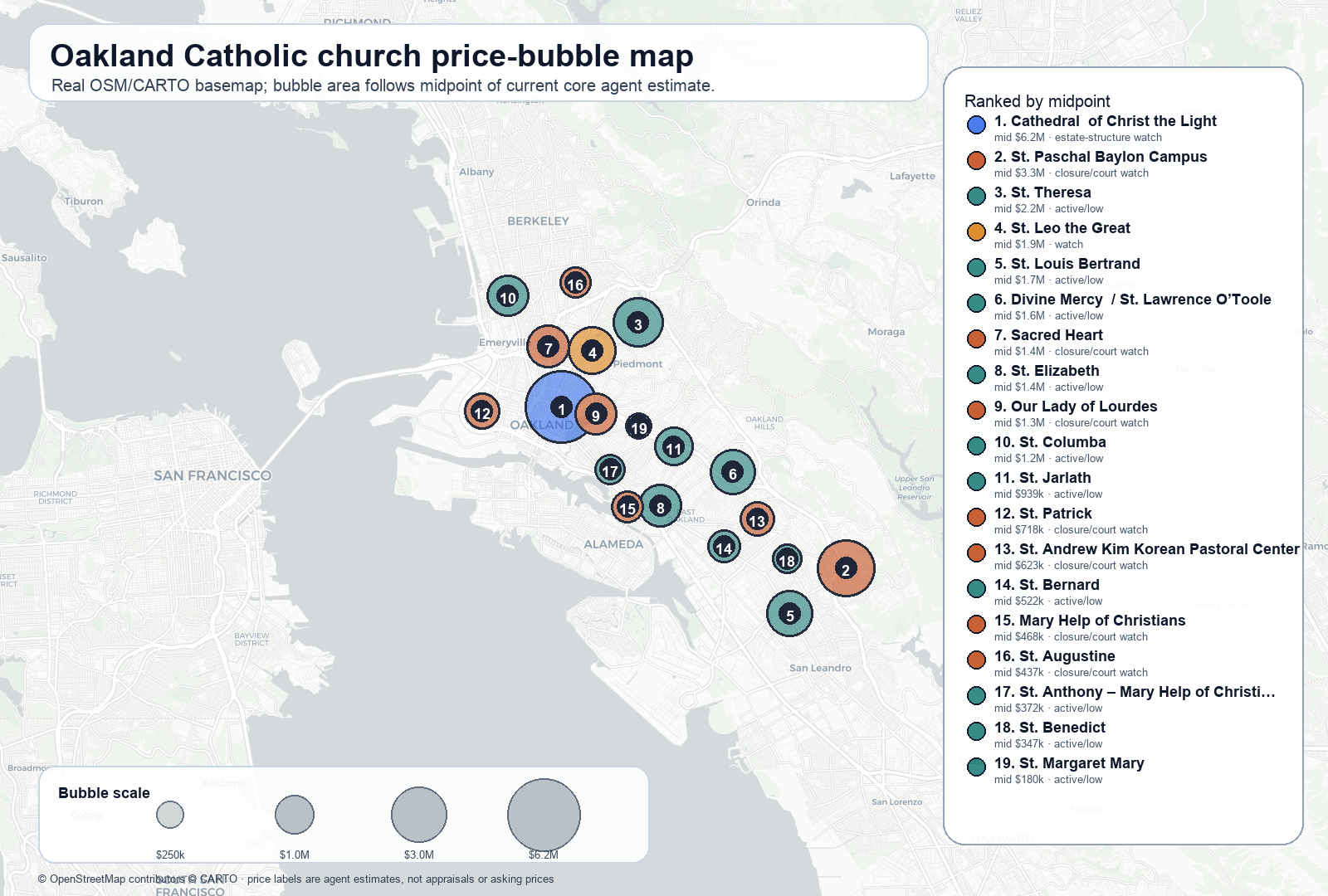

![]()

Research note as of 2026-05-14. This is not legal, tax, securities, lending, or land-use advice. It is a source-backed structure map: a way to identify which doors are real before anyone begins knocking on them with a checkbook and a dream.

Core finding

The strongest financing paths depend less on the romance of the church building and more on which legally legible public benefit the project can carry.

The practical hierarchy is:

- Affordable housing with community benefit — most fundable; gives access to public subsidy, CDFIs, SB 4, ACAH, CLT/co-op structures, possibly LIHTC/NMTC/HTC stacks; least compatible with a single individual’s desire for private control.

- Public arts / event / community facility — fundable through CDFIs, philanthropy, cultural-space models, NMTC in eligible tracts, grants for planning/capital, and earned revenue; entitlement and life-safety burden is serious.

- Individual live-work / residence — fundable if framed as a mixed-use or income-producing adaptive reuse, but pure owner-occupied residential use loses major subsidy channels, especially federal historic tax credits.

- Speculative private event venue — possible through SBA 504, IBank/CalCAP-style credit support, private equity, and Regulation Crowdfunding, but highest exposure to use-permit, assembly occupancy, alcohol, noise, parking, ADA/fire/seismic, and operating risk.

The elegant version of the project is probably not “buy a church, ask people to donate to my house.” That will trip private-benefit alarms. The fundable version is “preserve a neighborhood sacred/civic asset by putting it into a public-benefit ownership/use stack, while allowing a defined residential/live-work component to cross-subsidize the whole.” Less pithy, more bankable. Civilization is often an LLC with a good term sheet.

Scenario A — Individual wants to live there

A1. Private residence plus income-producing historic component

Structure:

- A single-purpose LLC acquires the property.

- The buyer occupies a defined residential unit or live/work portion.

- A separate income-producing component is created: event hall, studio rental, coworking, short-term class venue, office suites, or rental apartment(s).

- If the property can be certified historic, the income-producing portion may support federal historic rehabilitation tax credit planning.

- A historic consultant shapes the design to preserve character-defining elements, especially the sanctuary volume.

Why it could work:

- The federal historic tax credit is explicitly for income-producing certified historic buildings, not private owner-occupied residences. NPS states the 20% credit requires a certified historic structure, substantial rehabilitation, compliance with Secretary of the Interior’s Standards, and business/income-producing use.

- NPS eligibility guidance says private owner-occupied residences are ineligible, but rental residential and commercial use can qualify; a business/rental portion of a residence may be eligible only for that portion.

- The Oakland Melrose Baptist Church / Rose on Bond precedent is directly relevant: a 1930 Spanish Revival Oakland church complex was converted into 60 apartments; Heritage Consulting reports $12M cost and use of federal historic tax credits, while Connect CRE reports Chase historic tax credit equity and First Republic/Fannie-backed construction debt.

Source anchors:

- NPS, 20% Tax Credit Basics.

- NPS, Eligibility Requirements.

- Heritage Consulting, Melrose Baptist Church.

- Connect CRE, Historic Oakland Church Transformed into Multifamily Housing with Chase Investment.

Risks / constraints:

- Pure personal residence is a weak funding target.

- Historic tax credit structuring requires tax counsel, a historic consultant, and preservation-sensitive design.

- Church sanctuaries are hard: Novogradac/Heritage notes that NPS treats the sanctuary volume as character-defining; radically subdividing it is rarely approvable. Melrose initially tried to split the sanctuary into four apartments and had to instead create one oversized live-work unit.

- Change of use triggers Oakland planning/building review and likely certificate-of-occupancy, fire/life-safety, accessibility, seismic, mechanical/electrical/plumbing, and possibly parking/transportation questions.

A2. Renovation mortgage after residential legal path is established

Structure:

- Pre-close due diligence determines whether the property can become a 1-4 unit residential property or mixed-use primarily residential property.

- If plausible, explore FHA 203(k), Fannie Mae HomeStyle Renovation, or Freddie Mac CHOICERenovation after a lender confirms property eligibility.

- Use conventional acquisition/bridge/construction financing first if the building is not legally or physically mortgageable as residential at closing.

Why it could work:

- HUD 203(k) can finance acquisition plus rehabilitation in one mortgage for homes at least one year old, including single-family, 2-4 family, and mixed-use properties that are primarily residential, at least 51%.

- FHA Standard 203(k) supports major rehab, structural work, and conversion of a one-family structure to 2-4 units, subject to mortgage limits and process controls.

- Fannie HomeStyle and Freddie CHOICERenovation similarly bundle purchase/refi plus rehab, with as-completed appraisal mechanics and broad eligible improvements.

Source anchors:

- HUD, 203(k) Rehabilitation Mortgage Insurance Program.

- HUD, 203(k) Program Types.

- Fannie Mae, HomeStyle Renovation.

- Freddie Mac, CHOICERenovation Mortgages.

Risks / constraints:

- These are not magic “buy a church” products. The property and use have to fit residential/mixed-use underwriting.

- A church changing to residential likely needs planning approval before ordinary mortgage products become practical.

- FHA loan limits and habitability/draw rules may be misaligned with large sanctuary-scale rehab.

A3. Mills Act preservation residence

Structure:

- If locally historic or eligible, the buyer applies for an Oakland Mills Act contract.

- Property tax relief helps carry long-term maintenance in exchange for preservation obligations.

- Combine with a preservation plan, seismic scope, and public-facing preservation narrative.

Why it could work:

- California’s Mills Act is a property-tax incentive for qualified historic properties; local governments administer contracts, usually with a minimum 10-year term that runs with the land.

- Oakland has an active Mills Act program for qualifying historic properties and provides an application, model agreement, maintenance standards, and calculator.

Source anchors:

- California OHP, Mills Act Program.

- City of Oakland, Mills Act Tax Breaks.

Risks / constraints:

- Mills Act reduces carrying cost; it does not buy the building.

- The obligation runs with the land and limits future owner discretion.

- Oakland makes clear owners should consult legal/financial advisors.

A4. Friends-of-the-building nonprofit plus private residence — only if private benefit is cleanly separated

Structure:

- A 501(c)(3) or fiscal sponsor raises restricted funds for public/preservation portions only: façade, sanctuary public access, historical interpretation, community programming, preservation easement, or shared event hall.

- A private buyer funds the private residence portion and signs enforceable public-use/preservation covenants.

- Ideally use condominiumization, easement, long-term lease, or separate ownership of the public portion.

Why it could work:

- Donors will fund public benefit, not someone’s house.

- The building can become a “civic asset with a residence attached” rather than “residence with tax-deductible vibes.”

Potential funders / structures:

- National Trust Preservation Funds for planning/feasibility, not construction or acquisition.

- Local philanthropy for cultural preservation, if public access and equity narrative are real.

- Restricted donor gifts through a fiscal sponsor.

- Preservation easement donation if legally and economically viable.

Risks / constraints:

- Private benefit doctrine is the hard boundary. A nonprofit cannot raise charitable funds whose primary benefit is a private owner’s residence.

- Public access must be real, documented, insured, and operationally feasible.

A5. Small-business / venue house-hack

Structure:

- A for-profit event, hospitality, coworking, retreat, school, wellness, or arts business buys the church property.

- The business occupies/uses a majority of the building; the owner may have a residence or caretaker/live-work unit if zoning permits.

- Capital stack may include SBA 504, conventional bank debt, IBank/SBFC loan guarantee, CalCAP, private equity, and possibly Regulation Crowdfunding revenue-share notes.

Why it could work:

- SBA 504 finances long-term fixed assets including purchase, construction, and improvement of existing facilities, with up to $5.5M SBA loan amount, but requires an operating for-profit business and excludes passive/speculative rental real estate.

- IBank’s Small Business Finance Center supports loan guarantees for California small businesses and eligible legal entities, including not-for-profits; funds can support business expansion, construction, and working capital.

- CalCAP for Small Business supports lender loan-loss reserves; eligible uses include land acquisition, construction/renovation, startup costs, equipment, inventory, and working capital, subject to lender/program rules.

- Regulation Crowdfunding can raise up to $5M in 12 months through an SEC-registered portal, but it is a securities offering and carries disclosure/compliance constraints.

Source anchors:

- SBA, 504 Loans.

- IBank, Loan Guarantees.

- California Treasurer/CPCFA, CalCAP for Small Business.

- SEC, Regulation Crowdfunding.

Risks / constraints:

- Event businesses are operationally hard and permitting-heavy.

- Oakland entertainment venue rules can apply where the public is admitted, entertainment is provided, alcohol is served, dancing occurs, or late operation occurs.

- Insurance, ADA, fire, egress, noise, security, neighbor relations, parking, liquor licensing, and seismic work may dominate the pro forma.

Scenario B — Public event / arts / community space

B1. CAST-style cultural real estate trust

Structure:

- A nonprofit real estate trust or mission LLC buys or master-leases the church.

- Cultural/event tenants pay below-market rent under long-term leases.

- Tenant organizations build capacity over 7-10 years and may buy into ownership.

- Funding stack: CDFI acquisition debt + philanthropic PRIs/grants + capital campaign + possible NMTC/HTC + earned venue income.

Why it could work:

- CAST exists precisely to secure long-term affordable cultural space by acquiring/stewarding property and providing financial modeling, project management, and partnership development.

- Oakland already has precedent for CAST expansion: a $1.7M philanthropic investment from Kenneth Rainin and Hewlett supported CAST’s Oakland real-estate acquisition work and Keeping Space - Oakland technical/financial assistance.

- CounterPulse is the cleanest case: CAST formed an LLC, held a 90% managing stake while CounterPulse held 10%, used below-market rent and capacity-building, and after a seven-year NMTC timeline CounterPulse completed a $7M campaign to buy/renovate its home.

- Community Vision financed the Warfield Building acquisition with $7.3M in below-market acquisition financing for a CAST/KALW partnership creating long-term affordable space for arts, media, and nonprofits.

Source anchors:

- CAST, homepage / model.

- PRNewswire/Kenneth Rainin Foundation, $1.7M Oakland arts-space investment.

- Shelterforce, CounterPulse / CAST lease-to-own model.

- Community Vision, $7.3M Warfield acquisition financing.

Risks / constraints:

- Requires a credible anchor operator or coalition.

- Requires patient capital and capacity-building, not merely a purchase price.

- Needs a durable governance model so it does not become a beautiful insolvency machine.

B2. Community land trust / cooperative / CIT community ownership

Structure:

- A community land trust or permanent real estate cooperative acquires the church or land.

- The operating entity runs events, rentals, education, food, arts, or community programming.

- Community members buy modest shares or notes; residents/tenants participate in governance.

- The land/building is removed from speculative resale via ground lease, deed restrictions, or cooperative bylaws.

Why it could work:

- Oakland Community Land Trust stewards resident-controlled housing and community-serving real estate for permanent affordability.

- Artist Space Trust uses the CLT model to secure permanently affordable housing and creative space for Bay Area artists and culture-bearers.

- EBPREC’s West Oakland Esther’s Orbit Room/Cultural Arts Center used cooperative ownership plus a San Francisco Foundation $1.4M impact loan; SFF states EBPREC also raised project equity via a Direct Public Offering.

- Community Investment Trust offers a replicable neighborhood commercial real estate ownership model where local residents invest $10-$100/month, with education, dividends, and share appreciation.

Source anchors:

- OakCLT, homepage.

- Artist Space Trust, model.

- Northern California Land Trust, Artist Space Trust.

- San Francisco Foundation, $1.4M EBPREC / Esther’s Orbit Room impact loan.

- Community Investment Trust, model and about.

Risks / constraints:

- Community ownership is not free money; it is governance plus securities compliance plus operating competence.

- Direct public offerings / local investment notes require counsel.

- Small investors need plain-language risk disclosure and a plausible exit/repayment mechanism.

B3. NMTC + historic tax credit + CDFI community facility stack

Structure:

- Nonprofit or for-profit community facility project in an NMTC-eligible low-income census tract.

- CDE allocation provides New Markets Tax Credit financing.

- Historic Tax Credit equity is layered if the building is certified historic and rehab complies with NPS standards.

- CDFI/bank debt bridges acquisition and construction.

- Grants/capital campaign fill the gap.

Why it could work:

- NFF describes NMTC as equity-like financing for projects increasing community access to healthcare, education, arts, and workforce development.

- The Melrose Oakland precedent shows HTC equity can work for a former church when the design respects NPS constraints.

- Many Oakland church parcels may plausibly sit in NMTC-eligible low-income census tracts, but parcel-by-parcel confirmation is required.

Source anchors:

- NFF, Financing / NMTC.

- NPS, Tax Credit Basics.

- Heritage Consulting, Historic Tax Credits and the Adaptive Reuse of Churches.

Risks / constraints:

- NMTC deals are complex and usually too expensive for tiny projects unless bundled, highly impactful, or sponsored by an experienced CDE/CDFI.

- HTC and NMTC compliance periods constrain ownership and distributions.

- The project needs real community impact, jobs/services, and a qualified operating business/nonprofit.

B4. Public-private long-term lease / option model

Structure:

- Instead of purchasing immediately, the owner grants a long-term ground lease, master lease, or purchase option to a nonprofit/developer/operator.

- The operator raises renovation funds against long-term control.

- A public-benefit use covenant preserves community access.

Why it could work:

- Oakland’s Henry J. Kaiser Convention Center adaptive reuse is a local precedent: Oakland issued an RFP for a development team to rehabilitate, adaptively reuse, and operate a historic venue under a long-term lease; the developer, not the City, was responsible for raising funds and operating/tenanting the property.

- For church properties, this could be more plausible than outright sale if the Diocese wants continuing influence, preservation terms, or mission alignment.

Source anchor:

- City of Oakland, Henry J. Kaiser Convention Center Adaptive Reuse Project.

Risks / constraints:

- Long-term lease financing depends on lease term, assignment rights, lender protections, and owner consent to encumbrances.

- The owner must be willing to subordinate some control to make financing possible.

B5. Affordable housing plus sanctuary/community room

Structure:

- Nonprofit affordable housing developer, CLT, or co-op acquires or partners on the property.

- New housing is built on excess land or within secondary buildings.

- The sanctuary becomes a community/event room, chapel-like cultural space, childcare, food hub, performance space, or resident services center.

- Capital stack may include SB 4 streamlining, LIHTC, ACAH/Measure U funds, CDFI predevelopment/acquisition, HAF, and philanthropy.

Why it could work:

- SB 4 provides ministerial approval for 100% affordable housing on land owned by faith-based organizations and independent higher education institutions, effective July 2, 2024 through January 1, 2036, subject to criteria.

- Oakland ACAH provides acquisition and rehabilitation funding for nonprofit developers and CLTs; the 2025-2026 NOFA identifies up to $22M in Measure U funds administered through the Housing Accelerator Fund.

- Oakland has a live church-conversion affordable-housing precedent at 1433 12th Avenue / Brooklyn Presbyterian Church, approved for 32 affordable units with historic exterior preservation and a new four-story residential component.

- Buena Vista Terrace in San Francisco converted a historic church into 40 senior affordable apartments; sources included $7.9M from San Francisco Mayor’s Office of Housing, $5.1M HUD Section 202, and $320k Federal Home Loan Bank AHP.

Source anchors:

- HCD, SB 4 Affordable Housing on Faith & Higher Education Lands Act.

- City of Oakland, ACAH Funding.

- SFYIMBY, 1433 12th Avenue Oakland church conversion approved.

- ConstructConnect, Oakland church conversion for affordable housing.

- Affordable Housing Finance, Buena Vista Terrace church-to-senior-housing.

Risks / constraints:

- SB 4 appears strongest while a qualifying faith institution owns the land; a post-sale private owner may not qualify.

- Affordable housing stack is complex and slow, but it is the most subsidy-rich route.

- This path is poorly aligned with an individual buyer retaining private control.

B6. Active-congregation sacred-place grant bridge

Structure:

- If the congregation remains active or a mission-aligned congregation/community steward retains ownership, apply for sacred-place preservation grants and technical assistance.

- Use funds for urgent capital repairs and community-serving preservation.

Why it could work:

- The National Fund for Sacred Places provides matching grants of $50,000-$500,000 to congregations undertaking significant capital projects at historic houses of worship, plus training/technical assistance.

- Partners for Sacred Places also lists emergency/intervention funds up to $100,000 per congregation for short-term response, planning, and capital projects, invitation-only.

Source anchors:

- National Fund for Sacred Places.

- Partners for Sacred Places, Grant Opportunities.

Risks / constraints:

- These are for congregations / sacred-place stewards, not deconsecrated private acquisitions.

- Funds are meaningful gap fillers, not full acquisition capital.

Specific capital sources to approach or model

CDFIs and mission lenders

- Community Vision Capital & Consulting — California nonprofits/social enterprises; community facility, acquisition, rehab, construction, affordable housing; typical loans $250k-$5M, up to 90% LTV, terms up to 10 years. Source: Community Vision Lending.

- LISC Bay Area / LISC national — predevelopment, acquisition, construction, mini-perm, permanent, bridge, working capital; national loan-product ranges include $50k-$10M depending on product. Source: LISC Loan Products and LISC Bay Area lending.

- Nonprofit Finance Fund — bridge, lines of credit, predevelopment/construction, term loans, NMTC, and faith-based predevelopment loans for community-impact real estate. Source: NFF Financing.

- Housing Accelerator Fund / Oakland ACAH — if affordable housing, CLT, LEHC, or nonprofit preservation is part of structure. Source: Oakland ACAH.

- San Francisco Foundation Bay Area Community Impact Fund — precedent: $1.4M impact loan to EBPREC for West Oakland cultural/housing rehab. Source: SFF EBPREC loan.

Public and quasi-public credit support

- SBA 504 — for operating for-profit businesses purchasing/improving owner-occupied fixed assets; not passive real estate. Source: SBA 504.

- IBank Small Business Finance Center guarantees — California small-business credit enhancement, including legal entities and not-for-profits; supports construction and business expansion. Source: IBank Loan Guarantees.

- CalCAP for Small Business — loan-loss reserve support; eligible uses include land acquisition and building construction/renovation. Source: CalCAP SB.

Grants and philanthropy

- National Trust Preservation Funds — $2,500-$5,000 for planning/education, feasibility, expert reports; not acquisition/construction. Source: National Trust Preservation Funds.

- National Fund for Sacred Places — $50,000-$500,000 matching grants for eligible congregations with historic houses of worship. Source: Fund for Sacred Places.

- NEA Our Town — creative placemaking projects integrating arts/culture/design to advance community outcomes. Source: NEA Our Town.

- California Arts Council — general operating, impact projects, youth arts, cultural programs; usually not straightforward acquisition capital but useful operating/capacity support. Source: CAC Grant Programs.

- Oakland Direct Community Grant Program / CDE — Oakland-based nonprofits providing resident services aligned with racial equity goals. Source: Oakland Community Development Grants.

- Rainin / Hewlett / local arts philanthropy — direct Oakland precedent funding CAST’s Keeping Space - Oakland and acquisition fund.

Community investment / securities

- Regulation Crowdfunding — up to $5M in 12 months via SEC-registered intermediary; useful for revenue-share notes, preferred equity, or community ownership campaign, but requires securities counsel and ongoing disclosure. Source: SEC Regulation Crowdfunding.

- Direct Public Offering / cooperative shares — EBPREC precedent for community equity in West Oakland; must be structured under securities law.

- Community Investment Trust — resident investment model in commercial real estate with $10-$100/month investments, education, dividends, and share appreciation. Source: CIT.

Oakland permitting and entitlement constraints

Before any capital stack is credible, the project needs a parcel-level feasibility read:

- Oakland Planning & Building requires planning approval before building permits for changes to use, footprint, exterior, height, and historic resources. Source: Permit Process Overview.

- Additions, alterations, and conversions to habitable space require zoning review and building permits; housing projects may qualify for ministerial design review only if they do not require a CUP, variance, or development agreement. Source: Oakland additions/conversions.

- Oakland’s zoning map should be checked for each site: zoning district, height area, historic significance, General Plan designation, impact fee zone. Source: Oakland Zoning Map.

- Entertainment venue permits can apply to public-admission entertainment with alcohol, ticketing/dancing/late operations, venue rentals, live music, DJ events, comedy, pop-ups, and similar uses. Source: Oakland Entertainment Venue Permit.

- Special events have separate Oakland permitting. Source: Oakland Special Events & Permits.

Recommended deal prototypes

Prototype 1 — “Private live-work sanctuary, public cultural covenant”

Best for: an individual buyer with enough balance sheet to acquire, but who wants outside support for preservation/community uses.

- Buyer LLC acquires property.

- Historic consultant tests HTC eligibility.

- Sanctuary remains largely intact as event/studio/live-work space.

- Nonprofit/fiscal sponsor raises funds only for public/preservation improvements.

- Buyer grants public-access schedule, preservation easement/covenant, and possibly discounted rentals to local organizations.

- Funding: private equity/down payment + bank/construction debt + Mills Act + donor-funded public component + possible HTC only for income-producing portion.

Hard truth: this is legally delicate; private benefit must be policed like a proof obligation.

Prototype 2 — “CAST Oakland Sacred Spaces Fund”

Best for: public event / arts-space use.

- Create a dedicated acquisition vehicle with CAST-like governance or partner directly with CAST/community arts real estate actors.

- Bundle 2-4 church sites into a portfolio if one site is too small for NMTC/HTC economics.

- Anchor each site with a real operating tenant: arts org, childcare, food enterprise, rehearsal/performance operator, workforce nonprofit, or community college/education partner.

- Funding: CDFI acquisition line + PRIs from foundations + donor-advised fund capital + local capital campaign + tenant rent + grants.

Why this is promising: Bay Area precedent exists, Oakland precedent exists, and the public case is legible.

Prototype 3 — “Affordable housing on faith land plus preserved sanctuary”

Best for: sites with parking lots, school buildings, rectories, or excess land.

- Work before sale if possible, while faith ownership can trigger SB 4 eligibility.

- Partner with affordable housing developer / CLT / LEHC.

- Build affordable units on underused land or secondary structures.

- Preserve sanctuary as resident/community/event space.

- Funding: SB 4 entitlement streamlining + LIHTC + Oakland ACAH/Measure U/HAF + CDFI predevelopment + grants.

Why this is strongest: it is the most subsidy-rich. Tradeoff: the individual’s control claim mostly disappears.

Prototype 4 — “Cooperative cultural corridor node”

Best for: neighborhood-rooted event space and anti-displacement story.

- EBPREC-style cooperative or CLT acquires the asset.

- Local residents, artists, and supporters invest through compliant community offering.

- Use CDFI/foundation impact loan to cover acquisition/rehab gap.

- Operate as mixed-use venue: small stage, rehearsal rooms, rentable hall, kitchen/café, artist studios, nonprofit offices.

Why this is promising: it turns “other people fund it” into ownership and governance rather than donation. The moral geometry is cleaner.

Prototype 5 — “For-profit venue with community notes”

Best for: buyer/operator wants speed and control and accepts operating risk.

- For-profit venue company buys/leases the church.

- Use SBA 504/conventional debt if owner-occupied operating business qualifies.

- Use IBank/CalCAP credit enhancement if lender is hesitant.

- Raise Regulation Crowdfunding revenue-share notes from supporters for buildout.

- Set community programming commitments as brand/mission, not tax-deductible charity.

Why this is viable: it matches private control. Why it is risky: event-venue permitting, alcohol/noise/security, and debt service can eat the romance before dessert.

Priority next diligence

For each church parcel, build a one-page funding-readiness score:

- Historic status — National Register? Oakland landmark/heritage rating? Contributing district? Secular architectural significance?

- Zoning/use path — residential allowed? assembly/event allowed? CUP likely? entertainment/alcohol constraints?

- Physical risk — seismic, roof, ADA, sprinklers, egress, electrical, plumbing, environmental, deferred maintenance.

- Income model — units possible? event capacity? rental rates? anchor tenant demand? operating margin?

- Subsidy fit — SB 4, ACAH, HTC, NMTC, Mills Act, grants, CDFI, SBA/IBank/CalCAP.

- Governance fit — private LLC, nonprofit, CLT, co-op, fiscal sponsor, mission LLC, lease-option.

- Public story — preservation, affordable housing, arts displacement, Black cultural space, youth services, food access, workforce training, neighborhood gathering place.

- Speed — can it be optioned before full financing? Is seller willing to lease/option? Is a coalition ready?

Initial recommendation

Do not start with “Who will give money?” Start with three alternative pro formas and governance shells for one representative high-potential site:

- Private live-work + public covenant

- Nonprofit/CAST-style cultural facility

- Affordable housing + preserved sanctuary/community room

Then test each against the same parcel-level constraints: zoning, historic, rehab scope, revenue, subsidy eligibility, and operator credibility. The funders are downstream of that structure. Funders do not fund ambiguity; they fund a machine they can inspect.

Hourly deltas

2026-05-14 12:30 PDT — parcel-screening workflow and program mechanics

- Parcel subsidy screen should start with four official lookups, before pro forma romance begins. Use CDFI Fund CIMS for address/census-tract eligibility under NMTC and related CDFI Fund programs; Oakland’s Opportunity Zone page for the city’s 30 designated OZ tracts and city contact; Oakland’s zoning map for zoning district, height area, historic significance, General Plan designation, and impact-fee zone; and Oakland’s historic-property research page for permit records, BERD/State inventory, Oakland Cultural Heritage Survey files, NPGallery National Register nominations, CEQA/EIR history, Sanborn maps, and Oakland History Center records. Why it matters: the same church can be a strong NMTC/HTC/SB 4 candidate, a conventional private rehab, or a permitting tarpit depending on tract, historic flag, zoning/use path, and documentary history. Sources: CDFI Fund CIMS, CDFI mapping system, Oakland Opportunity Zones, Oakland zoning map, Oakland researching historic properties.

- SB 4 feasibility needs an industrial-buffer/environmental exclusion check, not just “faith-owned land.” HCD’s SB 4 guidance confirms 100% affordable housing, 55-year rental / 45-year ownership restrictions, urbanized-area and 75% urban-use perimeter tests, prevailing wage, and ministerial/CEQA-exempt review if criteria are met; it also excludes or constrains sites near heavy industrial, Title V industrial, refineries, hazards, wetlands, farmland, fault/flood areas, and conservation easements. Why it matters: Oakland church parcels near industrial corridors may fail SB 4 even when the ownership and affordability concept are right. Source: HCD SB 4 guidance PDF.

- LISC Bay Area has a faith-land capacity path that fits Oakland before a sale. Its Faith and Housing program has operated since 2019 for Bay Area faith/community organizations exploring affordable housing on owned land; the current application page describes a free one-year program with Learning Lab and Intensive Technical Assistance tracks, 9-county Bay Area eligibility, required site control/permission, board-level readiness, 8-10 hours/month staff time for intensive support, JV-partner guidance, modest predevelopment resources, and possible graduate forgivable loans up to $150,000 subject to funding. Contact listed: Evita Chavez,

echavez@lisc.org. Why it matters: this is a predevelopment/developer-partnering tool for a Diocese/congregation-owned site; it likely loses fit after a private buyer acquires the parcel. Sources: LISC Faith and Housing, LISC apply page. - NFF’s faith-real-estate pilot sharpens the predevelopment-loan option. NFF and Trinity Church announced a $1.5M Faith in Our Communities Fund in 2024 for flexible predevelopment loans and technical expertise for faith organizations using real estate for affordable housing or community development, backed by a Trinity credit guarantee; interest contact is

financing@nff.org. Why it matters: it is not acquisition equity for a private buyer, but it is a plausible early-stage runway source if the owning church/Diocese wants to evaluate mission-aligned reuse instead of making a hasty sale. Source: NFF / Trinity Faith in Our Communities Fund. - Oakland/HAF is now a faster affordable-housing acquisition channel, but only for the right borrower/use. Oakland’s ACAH/HAF materials identify up to $22M of Measure U funds for the 2025-2026 NOFA, administered by HAF, with Permanent Affordability and General Developer sub-programs for CLTs/LEHCs and nonprofit affordable housing developers. Oakland’s April 2026 partnership release says the city committed over $30M total, with $13.4M already committed to 110 affordable homes, and notes ACAH has preserved 312 units through 19 projects since 2017. HAF’s borrower page lists predevelopment, land acquisition, acquisition/rehab, construction, construction-to-perm, mini-perm, and permanent products, but says loans must benefit multifamily affordable housing in California. Why it matters: a church-to-housing project needs a CLT/nonprofit/developer borrower and multifamily affordability; a private live-work buyer should not count on this channel. Sources: Oakland ACAH, Oakland HAF partnership release, HAF borrower page.

- Arts/cultural gap capital is useful for operations and improvements, not purchase-price magic. Community Vision’s CREATE cohort is a two-year real-estate/financial readiness program for community-rooted arts organizations in Alameda and other Bay Area counties; applications are currently closed, but contacts are Amanda Bornstein and Sarah Schwid. Oakland’s Cultural Funding Program distributes over $1M annually and points arts nonprofits to the Arts Loan Fund; ALF lists secured loans at 3% as of March 2026, including bridge loans up to $50,000, case-by-case up to $100,000, facility-improvement loans, earned-revenue loans, and unsecured cash-flow loans at 3.5%. Why it matters: for a public venue, these can bridge grants, fund readiness, cash-flow events, or cover facility improvements; they do not replace CDFI/acquisition debt or a capital campaign. Sources: Community Vision CREATE, Community Vision resources, Oakland Cultural Funding Program, Arts Loan Fund loan products, Arts Loan Fund bridge loan.

- Negative evidence / timing caveat: San Francisco Foundation’s Bay Area Community Impact Fund remains a strong precedent source for EBPREC-style impact debt, but the current applicant page says the pipeline is fully allocated into FY27 and it is not taking new loan applications. Why it matters: cite BACIF as a model and possible future/donor conversation, not as immediately available 2026 acquisition financing. Source: SFF BACIF applicants.

2026-05-14 13:50 PDT — tract screen, state HTC, FHLBank, and term-sheet mechanics

- Preliminary subsidy geography now has a first tract screen for the 19 wiki-tracked Oakland Catholic sites. Using the wiki’s site addresses/coordinates, Census Geocoder tracts, CDFI Fund’s NMTC 2016-2020 ACS LIC file, and CDFI Fund’s current QOZ list, 11 of 19 screened addresses fall in NMTC low-income-community tracts and 7 of 19 fall in current Opportunity Zone tracts; 6 appear to overlap both: Mary Help of Christians, St. Andrew Kim Korean Pastoral Center, St. Anthony / Mary Help parish office, St. Benedict, St. Bernard, and St. Elizabeth. Sacred Heart is current-QOZ but did not screen as NMTC LIC; Cathedral, St. Columba, St. Jarlath, St. Louis Bertrand, and St. Patrick screen NMTC-LIC but not current-QOZ. Why it matters: this gives a first priority queue for NMTC/CDE and OZ-investor conversations, but it is not a parcel-boundary legal opinion; final eligibility should rerun from APN centroids/boundaries and the CDFI CIMS tool before term sheets. Sources: Census Geocoder, CDFI NMTC 2016-2020 ACS LIC file, CDFI designated QOZ list, CDFI CIMS.

- Opportunity Zone timing is now a 2026/2027 transition issue, not just a yes/no map layer. IRS/HUD guidance says OZ 1.0’s capital-gain deferral date ends December 31, 2026, while new designations and OZ 2.0 rules begin January 1, 2027; states can nominate eligible LIC tracts beginning July 1, 2026, and rural QOZs get enhanced rules that mostly will not help Oakland. Why it matters: for Oakland churches, current QOZ status may help frame investor outreach, but old-zone economics and new-zone designation risk should be modeled separately. Sources: IRS IR-2026-45, HUD OZ updates, CDFI Opportunity Zones resources.

- California’s State Historic Rehabilitation Tax Credit is an active extra preservation layer, but the pool matters. OHP’s SHRTC page describes California credits for eligible historic residential and income-producing properties: standard 20% of qualified rehabilitation expenditures, possible 25% enhanced credit, residential homeowner credits capped at $25,000, and the over-$1M QRE category currently marked exhausted/not accepting applications; CTCAC posts 2025 approved allocation rounds. Why it matters: this is a real add-on to federal HTC/Mills Act diligence for both a private live-work owner and an income-producing venue/housing structure, but a sanctuary-scale rehab may need to wait for future allocation capacity or fit into a smaller category. Sources: OHP State Historic Rehabilitation Tax Credit, CTCAC SHRTC allocations.

- FHLBank San Francisco gives two concrete non-generic grant lanes: AHP for affordable housing, AHEAD for economic/community development. AHP is member-bank submitted with a developer/community partner, requires subsidy need plus feasibility, at least 20% of rental units at or below 50% AMI, a 15-year rental retention period, and four years from award to complete/draw funds. AHEAD’s 2026 cycle has $10M allocated, maximum grant request $200,000, member-submitted applications for nonprofits/governments/Tribal organizations, and a May 27, 2026 deadline; housing projects eligible for AHP are not eligible for AHEAD. Why it matters: affordable-housing church reuse should add FHLBSF member-bank sponsorship to the LIHTC/ACAH/HAF list, while a public arts/community venue should test AHEAD for planning, jobs, training, small-business incubation, or activation costs rather than acquisition debt. Sources: FHLBSF AHP, FHLBSF AHEAD, FHLBSF AHEAD apply.

- The CAST-style model now has sharper term-sheet precedents. CAST/KALW’s Warfield Commons stack included a $7.3M purchase, equity from CAST and KALW, below-market Community Vision acquisition financing, a Kenneth Rainin Foundation-guaranteed capital-campaign bridge loan, and up to $17M in NMTC financing for improvements through the San Francisco Community Investment Fund. CounterPulse’s 80 Turk page/case study gives a smaller lease-to-own template: 9,418 sq ft, total development cost about $6.19M, CAST investment about $3.04M, NMTC about $1.86M, below-market rent around $0.51-$0.59/sf, a 90% CAST / 10% CounterPulse LLC, and a seven-year NMTC-linked buyout path. Why it matters: an Oakland church arts venue should not pitch “grants plus vibes”; it should pitch acquisition holdco, anchor tenant equity, below-market CDFI debt, guarantor-backed bridge, NMTC improvement financing, and a dated buyout/capacity-building schedule. Sources: CAST/KALW Warfield Commons, Community Vision Warfield financing, CAST CounterPulse case, CounterPulse 80 Turk.

- For a for-profit venue, the public-credit box is narrower than it first looks. SBA 504 can finance major fixed assets through CDCs but the borrower must be a for-profit operating business and loans cannot finance passive/speculative rental real estate; OCC’s SBA 504 overview gives the standard 50% bank / up-to-40% CDC / 10% borrower structure and notes 51% owner occupancy for existing buildings and 60% for new construction. CalCAP’s small-business loan-loss reserve can support land acquisition and building construction/renovation, but its summary lists bars, gambling facilities, and adult entertainment businesses as ineligible and caps enrolled support at $2.5M per borrower over three years. Oakland’s Entertainment Venue page adds practical friction: alcohol/public entertainment can trigger venue permits, with fee tiers around occupancy under/over 49 and separate extended-hours fees. Why it matters: a church venue with bar-like economics may lose CalCAP fit, while SBA 504 needs a genuine owner-user operating company rather than a passive venue-rental landlord. Sources: SBA 504, OCC SBA 504 overview PDF, CalCAP Small Business summary, Oakland Entertainment Venue permits.

2026-05-14 15:02 PDT — entitlement taxonomy, AHSC, NMTC allocation, and small-credit edges

- Oakland’s Planning Code gives a sharper first-pass use taxonomy for church reuse. Existing churches fall under Community Assembly Civic Activities, which explicitly includes churches/places of worship, nonprofit clubs/meeting halls/recreation centers, and community/cultural/performing arts centers. A private/for-profit event use may instead land in Group Assembly Commercial Activities if it is a theater/venue with 5,000+ sq ft of performance/lobby/audience area, cabaret/night club/dance hall/banquet hall, etc.; smaller instructional/theater uses can fall under Personal Instruction and Improvement Services Commercial Activities. Why it matters: the zoning diligence should not ask only “is assembly allowed?” It should classify the proposed operator as civic/nonprofit vs commercial, then check that activity and facility against the parcel’s zone table/CUP rules. The same sanctuary can be a fairly legible nonprofit cultural center and a much harder nightclub/banquet-hall entitlement. Source: Oakland Planning Code Title 17 PDF.

- Community Vision now has a fresh NMTC allocation to approach, not merely generic CDFI debt. Community Vision announced a $75M New Markets Tax Credit allocation in the 2024-2025 round, bringing its aggregate NMTC awards to $293M; the release frames the allocation for critical infrastructure in distressed California communities and lists Matias Bernal, VP of Development, as contact (

mbernal@communityvisionca.org). Why it matters: for NMTC-eligible Oakland church parcels, a public arts/community facility or mixed community-services project can ask Community Vision whether the site is large/impactful enough for allocation, whether it needs bundling with other sites, and what CDE impact metrics would make the deal financeable. Source: Community Vision NMTC allocation. - AHSC is a serious affordable-housing layer for church conversion, but it demands a transit/density/application-ready project. Round 10 materials describe roughly $750M available statewide, $10M minimum and $50M maximum per project, and up to $35M for affordable housing plus up to $15M for transportation/program costs. The SGC eligibility guide says AHSC can fund conversion of a non-residential building into affordable housing, but requires at least 20% affordable units up to 60% AMI, a 1/2-mile walk to transit, density thresholds, site control, discretionary land-use approvals/CEQA clearance by application deadline, and comparable-project experience. Round 10’s May 4, 2026 deadline has passed, so this is a next-cycle/next-coalition target. Why it matters: SB 4 + preserved sanctuary is not the whole housing stack; a transit-served Oakland church site with enough units could pair LIHTC/ACAH/HAF with AHSC if the developer locks site control and transit/bike/pedestrian partners early. Sources: HCD AHSC, SGC AHSC, SGC AHSC eligibility guide PDF, Round 10 guidelines.

- CalCAP Collateral Support is a distinct credit-enhancement tool for a for-profit venue, with the same “not a bar/passive real estate” warning light. The Collateral Support program can pledge cash to cover collateral shortfalls for eligible small-business loans, including purchase, construction, or renovation of an eligible place of business and bridge loans such as SBA 504 bridge financing; support is generally limited to the loan’s original term or five years, whichever is less. It excludes passive or residential real estate and prohibited activities including bars/liquor stores, adult entertainment, cannabis, gambling, tobacco, and firearms. Why it matters: if a private operator wants control, the cleaner model is an owner-user arts/event/production business with diversified revenue, not a passive hall-rental landlord or alcohol-led bar business. Sources: CalCAP Collateral Support summary, IBank loan guarantees.

- Oakland’s façade/tenant-improvement grant is small and currently closed, but it clarifies an edge case for a for-profit reuse. FTIP has offered reimbursement grants up to $30,000 façade, $45,000 tenant improvement, or $75,000 combined, including some ADA, permit/design, HVAC/plumbing/electrical/mechanical, hazardous-material abatement, signage, lighting, windows/doors, and historic-feature preservation costs. It is for property owners and independently owned for-profit business tenants; churches, nonprofits, chains, and franchises are listed as ineligible, and no work may start before a grant agreement. Why it matters: this is not acquisition capital, and it is not for a nonprofit arts steward, but if a for-profit venue/live-work operating company becomes the actual borrower/operator, future FTIP rounds could be a small finish-work or code-compliance gap filler. Source: Oakland FTIP.

- A preservation easement can sometimes make the “private owner plus public preservation” prototype more legally legible, but only if the historic test is real. California OHP’s federal easement guidance says charitable deductions can apply to partial interests in historic property donated for preservation purposes, and that for charitable-contribution purposes a certified historic structure need not be depreciable. Why it matters: this is one of the few tools that may still be relevant when a building includes private residential use, but it should be modeled as a restrictive covenant/easement with qualified donee, valuation, and IRS substantiation risk — not as a casual donor story. Source: OHP federal tax deductions / easements.

2026-05-14 16:48 PDT — faith-land mechanics, community equity, and renovation gap tools

- The Bay Area Faith and Housing model has a documented Alameda County playbook, not just a friendly brochure. A HUD case study says the LISC/EBHO program had supported 31 organizations since 2018, with a 12–18 month support cycle, $10,000 participation stipends, $10,000–$25,000 development coaches, up to $30,000 for preliminary design/feasibility, and LISC-developed forgivable loans to bridge the gap before public funding. Typical projects target households at or below 60% AMI, often use 55-year affordability terms, range from 4 to 104 units, and keep the faith/CBO owner in control through a ground lease or sale to a limited partnership. Why it matters: for SB 4 / affordable housing, the highest-value move is probably pre-sale engagement with the Diocese/congregation as land steward; after a private buyer closes, this lane mostly evaporates. Sources: HUD case study PDF, LISC Faith and Housing.

- Brooklyn Arms / 1433 12th Avenue now has a sharper predevelopment financing precedent. LIIF reports a $1M pre-construction unsecured revolving line of credit to Strive Real Estate for Brooklyn Arms Apartments; the current public description is 35 studios at 30% AMI plus a manager unit, with the adjacent former church rehabilitated for community space and property-management offices, and wraparound services expected with Alameda County Health Care Services Agency. Earlier SFYIMBY reporting described 42 affordable units, 12 inside the existing church, and a new four-story addition, so the unit count appears to have evolved. Why it matters: a local church conversion may need an early unsecured/pre-construction CDFI line before the final LIHTC/public subsidy closing; do not treat the first entitlement article as the final pro forma. Sources: LIIF Brooklyn Arms line of credit, SFYIMBY 2022 permit filing, PPM project note.

- The Kaiser / Oakland Civic case gives a concrete long-lease + tax-credit + community-benefits term sheet. KQED and East Bay Times describe Orton’s 215,000 sq ft Kaiser Convention Center reuse as roughly $64.5M, under a lease up to 99 years, with $3.1M in city grants, up to $20M in NMTCs, private equity/loans/tax credits, and community-benefit concessions after an appeal: up to 10,000 sq ft for small local nonprofits at about $2.00–$2.80/sf, lowest-published theater/ballroom rates for qualifying groups, an $80,000 annual production-cost endowment, $100,000 for Friends of the Calvin Simmons Theatre, and $75,000 for an anti-displacement fund. Why it matters: for a public church venue, “long-term lease” is financeable only when the lease is lender-grade and paired with enforceable access, rent, and governance commitments; the community-benefit schedule is not decorative frosting. Sources: KQED permanent-affordability report, East Bay Times renovation report, Oakland 2015 Kaiser RFP agenda report PDF.

- EBPREC’s community-equity example is a regulated cooperative security, not a casual donation jar with better typography. EBPREC’s Esther’s materials and SEC filing describe a Regulation A / Tier 2 direct public offering of Investor Owner Shares in the cooperative portfolio, not a project-specific Esther’s security: $1,000 shares, one-member-one-vote governance, target 1.5% annual dividend, non-transferability, a minimum five-year holding period before redemption, and explicit risk language that investors should be able to bear a complete loss. Next City reports the original Esther’s acquisition agreement at about $1.45M and notes non-accredited investors were capped by income/net-worth limits. Why it matters: an Oakland church co-op/CLT offering needs securities counsel and an offering architecture — Reg A/DPO, Reg CF note, California exemption, or private placement — chosen before public promotion begins. Sources: EBPREC Esther’s investor page, EBPREC SEC offering circular, Next City EBPREC DPO article, DFPI securities FAQ.

- There is a distinct renovation-gap stack for energy, electrification, and seismic work. Oakland says homeowners and commercial property owners can use approved PACE providers for energy efficiency, water efficiency, renewable energy, and EV chargers, and notes many PACE providers also finance seismic safety projects; CSCDA’s Open PACE platform explicitly includes energy, renewable, water-conservation, and seismic improvements, repaid through property-tax assessments. Oakland also points commercial owners to PG&E on-bill financing, whose current page lists 0% loans from $5,000 to $400,000, up to $6M by exception, with terms up to 120 months; GoGreen Business financing can reach $5M for qualifying small businesses. Why it matters: this does not buy the church, but it can carve expensive MEP/electrification/seismic scopes out of the acquisition loan or capital campaign — subject to mortgage-lender consent, assessment-lien priority, and eligible-measure engineering. Sources: Oakland Clean Energy Financing, CSCDA Open PACE, Oakland commercial electrification resources, PG&E Energy Efficiency Financing.

- Nonprofit venue rentals need UBIT structuring before anyone builds the “community event hall” spreadsheet. IRS guidance says rent from real property is generally excluded from unrelated business taxable income, but the exclusion can fail for substantial services to occupants, mixed personal-property leases, net-profits rent, controlled-entity issues, or debt-financed property; the general UBI test is trade/business, regularly carried on, and not substantially related to exempt purpose. Why it matters: a nonprofit/CLT/faith steward should model fixed/gross rent, mission-related programming, separate taxable subsidiaries where needed, and debt-financed-property exposure before relying on event, bar, parking, catering, or equipment-rental income. Sources: IRS rent-from-real-property UBTI exclusion, IRS debt-financed property UBI, IRS unrelated business income defined.

- The National Fund for Sacred Places is a better active-congregation capital-campaign catalyst than a post-sale rescue source. The 2026 cycle accepted applications January 13–March 3, with roughly 30–40 grantees selected in October; program materials emphasize $50,000–$500,000 capital grants, a 1:1 cash match, envelope/structural needs before interior or ADA work, Secretary of the Interior Standards, 100% construction documents and 25% of matching funds raised before capital-grant submission, and possible $20,000 planning grants for accepted participants. The Intervention Fund separately offers up to $100,000 with no cash match for unanticipated emergencies, by invitation only. Why it matters: if a parish/Diocese keeps ownership long enough to steward preservation and community use, this can de-risk urgent building work; a deconsecrated private live-work acquisition should not underwrite against it. Sources: National Fund apply page, National Fund what we offer, National Fund FAQ, Intervention Fund.

2026-05-14 18:26 PDT — code, property-tax, accessibility, and seismic gap filters

- Qualified historic status is not only about tax credits; it can change the building-code negotiation through the California Historical Building Code. OHP says the CHBC provides alternative building regulations for repairs, alterations, additions, change of use, and continued use of a “qualified historical building or structure”; ICC’s CHBC text says city/county enforcing authorities apply those alternative standards for qualified historic buildings, but the building must be recognized by an appropriate local or state jurisdiction/register/inventory. Why it matters: for a church with sanctuary volume, older stairs, seismic constraints, and accessibility conflicts, the first diligence question should be “can this qualify for CHBC treatment?” alongside HTC/Mills Act—not as a safety waiver, but as a preservation-aware code path for both a private live-work reuse and a public venue. Sources: OHP State Historical Building Code, DGS California Historical Building Code, ICC 2022 CHBC Part 8.

- The live/work box is much smaller than “I live in the sanctuary and sometimes host things.” The 2022 California Building Code live/work rule classifies compliant live/work units as Group R-2 and limits each unit to 3,000 sq ft, no more than 50% nonresidential area, nonresidential use on the first/main floor only, and no more than five nonresidential workers at one time; it also ties egress, occupant load, sprinklers/fire alarm, structural loads, accessibility, ventilation, and plumbing to the function served. Oakland Building Directive 21-02 adds a local interpretation for joint live-work sleeping lofts in existing buildings, but its background is commercial/industrial adaptive reuse and its loft guidance assumes sprinklers/EERO constraints. Why it matters: an individual buyer should not underwrite a whole church as one simple live/work unit; the cleaner plan may require a conventional dwelling unit plus separately permitted assembly/studio/business areas, or multiple units/uses with explicit occupancy separations. Sources: ICC 2022 CBC Chapter 5 / Section 508.5, DGS code-cycle page, Oakland Building Directive 21-02 PDF.

- For nonprofit/CLT/co-op ownership, California property-tax exemption is a real carrying-cost lever with its own proof obligations. BOE’s Welfare Exemption guide says 501(c)(3) status is not enough: the organization needs an Organizational Clearance Certificate from BOE and the county assessor separately determines exempt property use; formation documents need irrevocable-dedication/dissolution language, annual county filings are required, and shared use may need additional forms. BOE’s low-income housing page adds that nonprofit/LLC owners can have unlimited assessed-value exemption when the property receives LIHTC or government financing, while limited partnerships need both an OCC for the managing general partner and a property-specific Supplemental Clearance Certificate, plus government financing or tax credits. Oakland separately exempts some city special assessments for nonprofits/affordable housing when a paid Oakland business license and Alameda County Welfare Exemption proof exist, with annual refiling and a May 15 early deadline. Why it matters: a public venue or affordable-housing church reuse should model property-tax exemption and special-assessment relief as part of the operating stack; a private buyer, for-profit venue, or sloppy mixed private-benefit use should assume taxable carrying costs until counsel proves otherwise. Sources: BOE Property Tax Welfare Exemption PDF, BOE low-income rental housing welfare exemption, BOE nonprofit exemption resources, Oakland property-tax exemptions/refunds.

- ADA/accessibility work has a small but concrete financing/tax-credit stack for an operating business. CalCAP ADA Retrofits is a loan-loss-reserve credit enhancement for participating lenders making loans up to $50,000 for ADA retrofits/alterations, including CASp surveys, estimating/planning, and physical retrofit work; the Treasurer lists

calcap@treasurer.ca.govfor program questions. IRS guidance says eligible small businesses with $1M or less in receipts or no more than 30 full-time employees can use the Disabled Access Credit each year they incur access expenditures, and businesses of any size may deduct up to $15,000/year for qualified architectural/transportation barrier removal; the two can be combined when requirements are met. Why it matters: this will not solve sanctuary-scale rehab, but for a for-profit venue/live-work business or nonprofit’s taxable affiliate it can finance and partially offset CASp-driven door/restroom/path-of-travel fixes—the unromantic little hinges on which public use often turns. Sources: CalCAP ADA Retrofits, CalCAP ADA small-business information, IRS disability-access tax benefits, IRS accessible-business tax benefits, DGS five steps for business accessibility PDF. - Seismic/hazard mitigation grants are a possible public/nonprofit partner lane, not private acquisition capital. Cal OES’s Hazard Mitigation Assistance page lists HMGP rolling applications as open, identifies private nonprofits as eligible for HMGP/HMGP Post-Fire subapplicant treatment, and gives

resilientca@caloes.ca.govfor technical assistance; FEMA’s HMGP page says homeowners and businesses cannot apply directly, though local communities may apply on their behalf, and mitigation-plan and cost-effectiveness requirements apply. FEMA’s BRIC page also shows a combined FY2024/2025 opportunity with a July 23, 2026 application deadline and evaluation/EHP/BCA support channels. Why it matters: if a sanctuary must carry a major seismic or flood/hazard scope, the actionable route is a city/county/nonprofit hazard-mitigation subapplication or public-benefit facility framing; a private live-work buyer should not count this as closing capital. Sources: Cal OES HMA grants, FEMA HMGP, FEMA BRIC.

2026-05-14 20:37 PDT — seller approvals, tax-credit lease traps, resilience-center grants, and venue filters

- The closure/sale funnel is now explicit for seven Oakland sites, so acquisition outreach should model seller-process risk. The Diocese’s April 28 MAP announcement lists Mary Help of Christians, Our Lady of Lourdes, Sacred Heart, St. Andrew Kim Korean Pastoral Center, St. Augustine, St. Paschal Baylon, and St. Patrick as Oakland closure sites; it also says parish property/goods do not belong to private individuals and that disposition of sale proceeds will be handled with the receiving pastors. The Oaklandside’s follow-up says the property-sale path will be unique to each site and has no exact timeline. Why it matters: an LOI/option/lease pitch should be parcel-specific, conditional on diocesan and bankruptcy-process approvals, and fast enough to preserve SB 4 / faith-land possibilities before a fee-simple private sale closes. Sources: Diocese MAP announcement, Oaklandside closure report, Diocese Chapter 11 page.

- Canon-law approval thresholds are a real term-sheet issue for long leases, options, debt, and sales. USCCB complementary norms say diocesan acts of extraordinary administration can require consent of the diocesan finance council and college of consultors; alienation thresholds depend on diocesan Catholic population, with maximum limits of $7.5M for dioceses with at least 500,000 Catholics and $3.5M for others, and lower minimum thresholds. For leasing diocesan property, the bishop must hear the finance council and college of consultors when market value exceeds $400,000 and must obtain their consent when market value exceeds $1M or the lease term is three years or longer; public juridic-person leases above $5M require Holy See consent. Why it matters: the Kaiser-style long lease, CAST-style lease-to-own, and SB 4 ground-lease paths may be more financeable than a purchase, but they are not pastor-handshake instruments. Put approval contingencies, outside dates, and assignment/lender-protection language in the first serious term sheet. Source: USCCB Complementary Norms, canons 1277, 1292, 1297.

- Historic Tax Credit stacks with nonprofit, faith, CLT, or public tenants need tax-exempt-use engineering before the operating plan hardens. IRS rehabilitation-credit guidance warns that property used by tax-exempt entities generally does not generate the credit unless an exception applies, and its tax-exempt-use guide flags disqualified leases involving tax-exempt financing, fixed-price purchase options, lease terms over 20 years, and sale-leaseback facts. Novogradac’s HTC leasing note adds the practical instruction: track all tax-exempt tenant floor area cumulatively and draft renewal options at fair-market value when possible. Why it matters: the attractive CAST/NMTC/HTC story can break if a nonprofit anchor tenant receives the wrong long lease or buyout option. Treat lease architecture as part of the tax-credit design, not an afterthought scribbled on the napkin after the architect has already fallen in love. Sources: IRS rehabilitation credit FAQ, IRS tax-exempt-use guide PDF, Novogradac HTC tax-exempt lessee considerations.

- A church-as-resilience-center frame opens a different public/community venue grant lane. California SGC’s Community Resilience Centers Round 2 guidelines show roughly $55M available, with planning grants of $100k-$500k and implementation grants of $1M-$10M for eligible 501(c)(3) nonprofits, public/local agencies, tribes, utilities, and similar public-benefit leads. Implementation projects can fund construction, retrofits, land acquisition, and year-round programming, but must satisfy partnership, priority-community, emergency-function, evaluation, and 15-year facility-use-commitment requirements. Why it matters: for a public event/community venue, the sanctuary can be pitched not only as arts space but as a climate/emergency resilience hub with backup power, cooling/air filtration, food/water capacity, broadband, and trusted CBO programming. This is structurally useless to a private residence, and rather useful to a nonprofit/CBO/city partnership. Sources: SGC Community Resilience Centers, CRC Round 2 final guidelines PDF.

- Venue feasibility should split occupancy classification from Oakland’s entertainment/special-event permits. The 2022 California Building Code classifies churches and many community halls/galleries as Group A-3, theaters/concert halls as A-1, food/drink/nightclub uses as A-2, and assembly spaces with occupant load under 50 as Group B. Separately, Oakland’s entertainment venue rules can apply when the public is admitted, entertainment is provided, and alcohol is served, or where public/no-cover dancing plus alcohol runs after 11 p.m.; the city lists live music, DJs, comedy, karaoke, fashion shows, sip-and-paint, pop-up food events, outside-promoter events, venue rentals, public parties, and ticketed events. Oakland special-event permits can also apply to public, advertised/ticketed gatherings of 50+ with entertainment and alcohol, and outdoor amplified sound has its own permit. Why it matters: the pro forma should not use one blended “event revenue” line. A sober nonprofit A-3 community hall, a 49-person arts studio, a 300-person ticketed concert hall, and an alcohol-led nightclub are different entitlement, fire, insurance, police, ADA, and neighbor-noise animals. Sources: 2022 California Building Code Chapter 3, Oakland Entertainment Venue permit, Oakland Special Event Permit, Oakland Sound Amplification Permit.

- Do not assume the church’s ADA religious exemption survives the reuse. DOJ’s Title III manual says religious entities and their facilities are exempt from Title III, but a private entity renting a congregation’s facility to operate a public accommodation is not exempt unless it is itself religious; the manual also warns that public-accommodation landlord and tenant duties cannot simply be assigned away as against disabled patrons. Why it matters: once a nonreligious venue operator, café, school, coworking studio, or arts nonprofit runs public-facing uses, the diligence budget should include CASp review, path-of-travel, restrooms, seating, ticketing/communication accommodations, and lease allocation of who pays. Source: DOJ ADA Title III Technical Assistance Manual.

- For a for-profit live-work/venue business, call SBA 504 CDCs early rather than treating 504 as a generic bank product. SBA says 504 loans are available exclusively through Certified Development Companies; Bay Area Development Company and TMC Financing are concrete California/Bay Area CDC-style starting points. BayDevCo’s 504 summary gives the useful underwriting skeleton: 50% conventional first lien, 40% SBA/CDC second lien, usually 10% borrower equity, 51% owner occupancy for existing buildings, 60% initial occupancy for new construction, and 15% down payment if the company is a startup or the property is special-purpose. Why it matters: a private venue operator should pre-screen whether a former church will be treated as special-purpose collateral and whether the operating company can occupy enough space; if the model is passive hall rental with alcohol-led economics, the 504/CalCAP thesis weakens quickly. Sources: SBA CDC directory, Bay Area Development Company 504, TMC Financing.